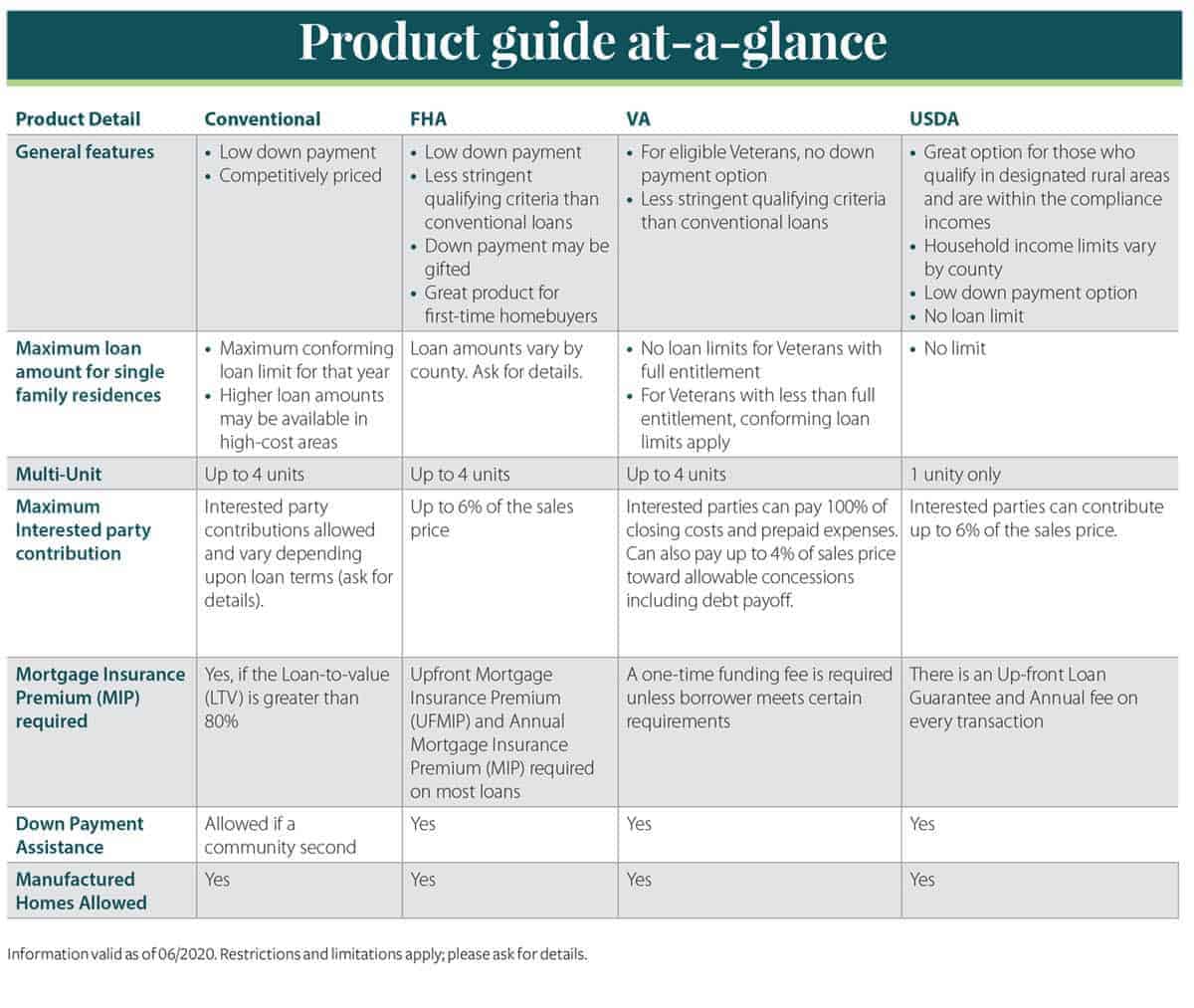

Home Purchase

At Evergreen Home Loans, we offer a range of highly affordable loan programs for first-time homebuyers including those with low down payment plans or 100% financing programs. Ready to get started? We recommend these simple steps:

- Get your preapproval* at Evergreen. It’s a good idea to start the preapproval process before you shop. That way you know how much home you can afford.

- Be prepared. Shop with confidence with our Security Plus Seller Guarantee®. If you qualify, we provide a fully-approved loan amount and guarantee it or we pay your seller $5,000.** It puts buyers in the strongest position possible when competing with multiple buyers for homes.

- Work with a real estate professional. A real estate professional can help you find homes you can afford while helping you prioritize all those features that make a house a home. If you need help in finding a qualified professional, just ask us. We’re happy to provide recommendations.

Rent vs. Own Myths and Facts

MYTH: You need a lot of cash to buy a home.

FACT: There are many loan programs available with options to alleviate needing a lot of cash to buy a home. Many financing options exist such as, down payment assistance programs and low-to-moderate income programs for buyers that may need some additional help.

MYTH: Home loan monthly payments are not affordable.

FACT: A variety of loans offer options for lower monthly payments making homeownership more affordable.

MYTH: You need a FICO score in order to qualify for a home loan.

FACT: A FICO score isn’t necessary to qualify. “Alternative” sources of credit ratings such as utility bills, cell phone, gym membership, rent, etc. may be considered with certain loan types.

MYTH: You need perfect credit to qualify for a home loan.

FACT: Perfect credit is not needed to secure approval for a home loan. While credit scores can range widely, the higher your credit score, the more options you will have to find a home loan with favorable interest rates.

MYTH: You need to have had the same job for many years to qualify for a home loan.

FACT: Changing jobs doesn’t automatically disqualify you. If you stay in the same line of work for a period of time, lenders will factor that into the qualifying criteria.

MYTH: Today’s housing market is the wrong time to buy a home.

FACT: Today’s housing market offer great opportunities to purchase a home. With current low rates and the right tools like our Security Plus Seller GuaranteeTM, first-time homebuyers will be prepared with buying power.

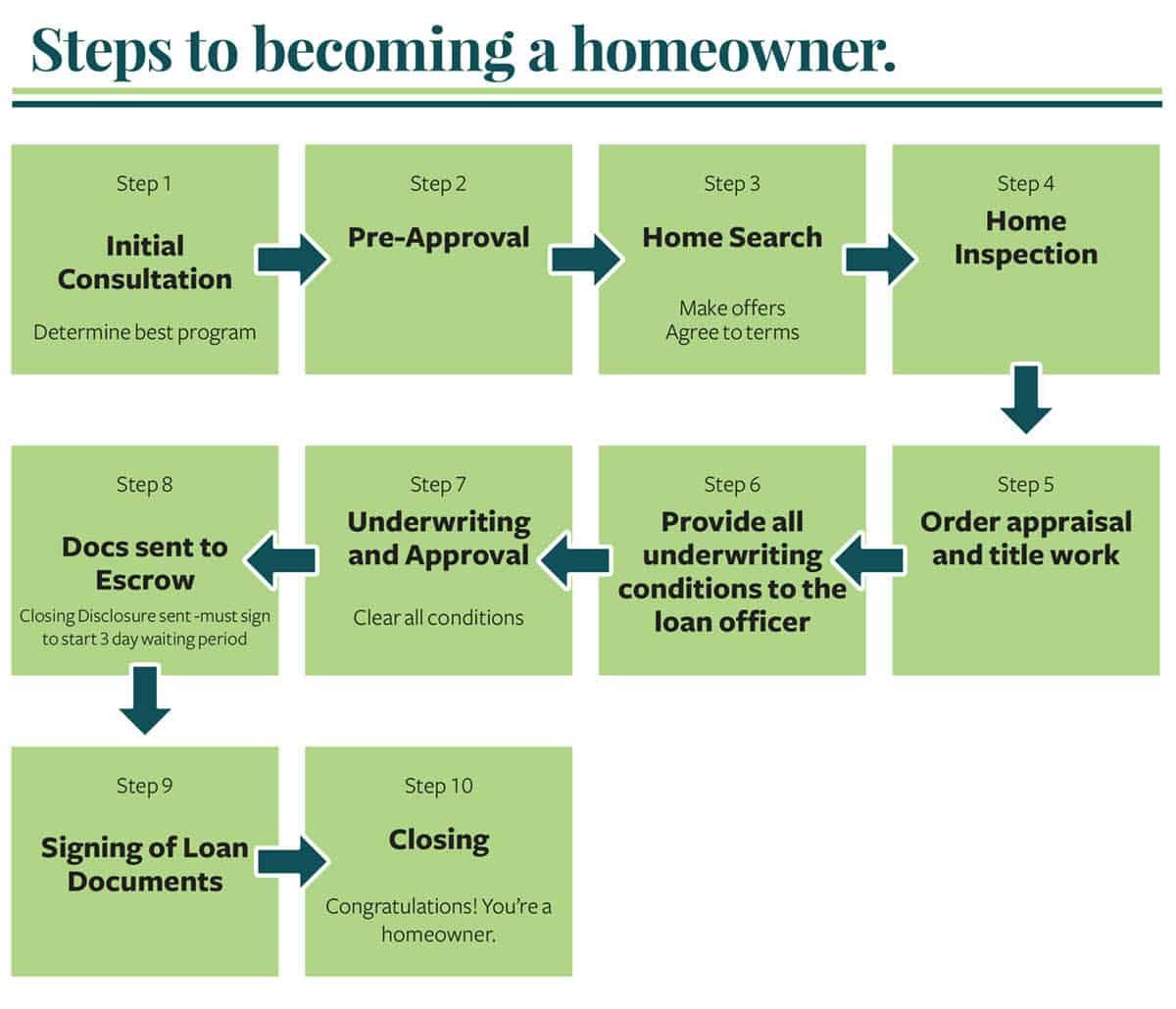

The steps below are an example of a typical home loan process. Depending on your personal circumstances, there may be more or less steps required.

Home Loan Terminology

Annual Percentage Rate (APR)—The cost of credit over the life of the loan. This includes the interest rate, closing costs, discount points, and other fees associate with the loan.

Appraisal—A professional opinion on the value of the home and property using factors such as the selling price of similar homes and overall quality of the property. An appraisal will not check the functionality or condition of a home.

Discount points—Fees paid to the lender at closing to reduce the interest rate. One point equals one percent of the loan amount. For example, one point on a $100,000 loan would equal $1,000.

Down payment—A percentage of the property purchase price that is paid at closing.

Earnest money—A deposit made to the seller representing the buyer’s good faith to purchase the home. At closing, the funds go towards the down payment and closing costs.

Interest rate—The amount the lender charges for lending money. Typically expressed as a percentage.

Mortgage insurance (MI)—This insurance lowers the risk for the lender when making a loan and may be included on some loan types. If a loan includes mortgage insurance, the cost could be included in the total monthly mortgage payment, due at closing, or both. Mortgage insurance can be removed in the future after the mortgage balance reaches a certain percentage.

Origination fee—The fee the lender charges to process the loan.

Preapproval1—An estimate from the lender of the amount of financing a potential borrower is approved for. The lender often looks at credit, income, and assets to determine this number. Keep in mind a preapproval is not an approval. The loan will still need to go through underwriting for final approval.

Prequalification—An estimate from the lender of how much financing a borrower could secure. This amount is often based on limited documentation or information verbally disclosed to the lender. It may provide a good idea of how much home they could afford, however is not a firm estimate.

Principal—The amount borrowed from the lender that the borrower is responsible for paying back.

Security Plus Seller Guarantee®—A program from Evergreen that will preapprove a customer with a fully underwritten loan amount. We guarantee financing or we’ll pay the seller $5,0002 for their time. This powers up purchase power and can help homebuyers stand out in a competitive market.

Underwriting—An analysis to determine whether the risk of lending money is acceptable to the lender. It involves evaluating the property and the borrower’s ability to repay the loan.

- Preapproval is not a commitment to lend and is subject to satisfactory loan conditions including a completed application and property appraisal. Other terms and restrictions apply. Not all products available.

- Applies to purchase loans only. To qualify, buyer’s Security Plus Approval/Seller Guarantee Addendum must have been issued by Evergreen and the Seller shall have executed the addendum with their signature. Certain loan types do not qualify for this offer. Restrictions apply.